The $1.2 Trillion Burden: Why Americans Are Drowning in Credit Card Debt

American households are collectively shouldering a staggering $1.2 trillion in credit card debt, a number that paints a stark picture of the financial pressures facing families across the nation. But contrary to the image of reckless spending, much of this debt isn’t fueled by lavish purchases. Instead, it’s the accumulation of everyday expenses – car repairs, unexpected medical bills, and even basic groceries – that are pushing people deeper into the red. The high interest rates associated with credit cards, coupled with the compounding effect of minimum payments, are creating a debt trap that’s increasingly difficult to escape.

The Perfect Storm: High Rates and Stagnant Wages

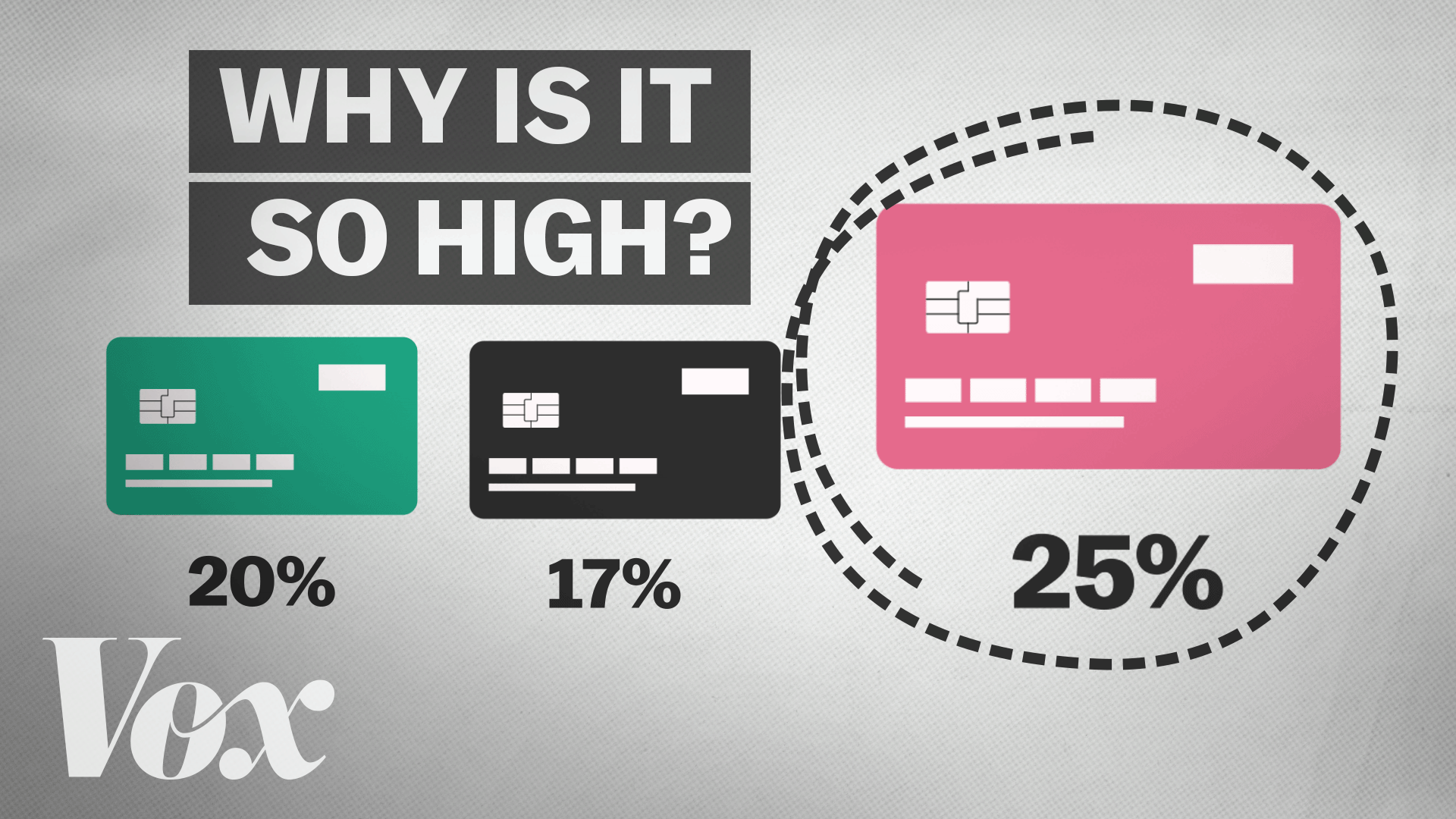

The average credit card interest rate is currently hovering around a concerning 20%, nearly double what it was in 2010. Several factors contribute to these elevated rates. Firstly, the Federal Reserve’s efforts to combat inflation by raising interest rates have a direct impact on credit card APRs. However, this is only part of the explanation. Credit cards are unsecured loans, meaning lenders bear a greater risk as they lack collateral to seize in case of default. This inherent risk is reflected in the higher interest rates.

Furthermore, the increasing reliance on credit cards underscores a broader economic challenge: wage stagnation. As wages fail to keep pace with the rising costs of living, particularly in sectors like healthcare, more Americans are turning to credit cards to bridge the gap between income and expenses. This dependence creates a vicious cycle, as the interest payments on credit card debt further strain household budgets, making it even harder to achieve financial stability.

Breaking Free From the Cycle: Strategies for Debt Management

Escaping the credit card debt trap requires a multi-pronged approach. Consumers need to be vigilant about tracking their spending, prioritizing debt repayment, and exploring options such as balance transfers to lower-interest cards or debt consolidation loans. Financial literacy and responsible credit card usage are also crucial. However, individual actions alone may not be enough. Systemic solutions, such as policies that address wage stagnation and healthcare affordability, are needed to alleviate the financial pressures that drive people into debt in the first place.

In conclusion, the current credit card debt crisis is a complex issue stemming from a confluence of economic factors. While responsible financial management is essential, addressing the underlying economic pressures is crucial for creating a more sustainable and equitable financial landscape for all Americans.

Based on materials: Vox